OVERVIEW

The purpose of this document is to provide detail around the current operating model approach of Wealth Management businesses, its service offerings, and an I.T strategy to transition to a future state that will lead to:

- Greater automation for the operational team, improved efficiencies

- Customer journey improvements, more seamless

The operating model is the necessary level of business process integration and standardization for delivering goods and services to customers, which can be the enabler for growth.

There are Four Types of Operating Models:

1. Diversification (low standardization, low integration)

2. Coordination (low standardization, high integration)

3. Replication (high standardization, low integration)

4. Unification (high standardization, high integration)

Characteristics of the four operating models

| Coordination – Shared customers, products, or suppliers’ impact on another business unit transactions – Operationally unique business units or functions – Autonomous business management Business unit control over business process design – Shared customer/supplier/product unit data – Consensus processes for designing IT infrastructure services; IT application decisions made in business units | Unification – Customers and suppliers may be suppliers of local or global – Globally integrated business processes often with the support of enterprise systems business units with similar or overlapping operations – Centralized management often applies functional/process/business unit matrices – High-level process owners design standardized processes – Centrally mandated databases decisions made centrally |

| Diversification – Few, if any, shared customers or suppliers Independent transactions – Operationally unique business units – Autonomous business management Business unit control over business process design – Few data standards across business units – Standardized data definitions but data – Most IT decisions made within business units | Replication – Few, if any, shared customers Independent transactions at a high level – Operationally similar business units – Autonomous business unit leaders with limited discretion over processes – Centralized (or federal) control over business process design – Few data standards across the business – Standardized data definitions but data locally owned with some aggregation at corporate – Centrally mandated IT services |

To decide which quadrant your company (or business unit) belongs in, ask yourself two questions:

- To what extent is the successful completion of one business unit’s transactions dependent on the availability, accuracy, and timeliness of other business units’ data?

- To what extent does the company benefit by having business units run their operations in the same way?

The first question determines your integration requirements; the second is your standardization requirements.

What operating model you choose will drive important design decisions around the autonomy of business unit managers and the role of IT.

Case Study For Wealth Management Businesses

Company Name: Merrill Lynch Global Private Client

Operating Model: Coordination

- Single face to the customer through multiple channels

- Individual financial advisers own their customer relationships

- Financial advisers customize their interactions with customers

- Financial advisers in 630 offices exercise local autonomy within the bounds of their responsibilities in management

- Total Merrill platform provides shared access to technology and data

- IT organization provides centralized technology standards

Different operating models position companies for different types of growth, for Coordination it provides the following opportunities for growth:

- Organic: stream of products of innovations easily made available to existing customers using existing integrated channels

- Acquisition: can acquire new customers for existing products but must integrate data.

An operating model helps define the range of strategic initiatives a company can readily pursue. As long as the operating model presents attractive options, it provides a stable approach to delivering goods and services.

Shifting from one operating model to another is transformational. A transformation disrupts a company, imposing new ways of thinking and behaving.

The operating model, once in place, becomes a driver of business strategy.

WEALTH MANAGEMENT TRENDS

While some organizations may choose the cost-cutting route, others will point toward smarter execution, finding ways technology can be deployed to add value and create superior customer experiences.

2023 could be the year the “new normal” fully come into view. There will be opportunities to help define the future, one in which profits and purpose are inextricably linked. Financial services leaders can be poised and ready to move the industry forward

Firms continue to invest in digital transformation with new technologies that improve the client experience, gain operational efficiencies, and potentially generate alpha. The connection between progress on the digital transformation journey and improving culture is remarkably strong.

Client-centricity is also gaining importance. Firms focusing on client-centricity should also rethink fund distribution through integration and collaboration with digital platforms. Furthermore, governance and reporting mechanisms at many investment management firms have still not caught up with the pace of digital transformation.

Digitization with a twist

The companies that will be successful in the fourth industrial revolution will be those that understand the drivers of value, such as data, artificial intelligence, machine learning, digitization, and eCommerce). We are currently in the era of platforms giving the business owner the ability to launch their business into multiple ecosystems

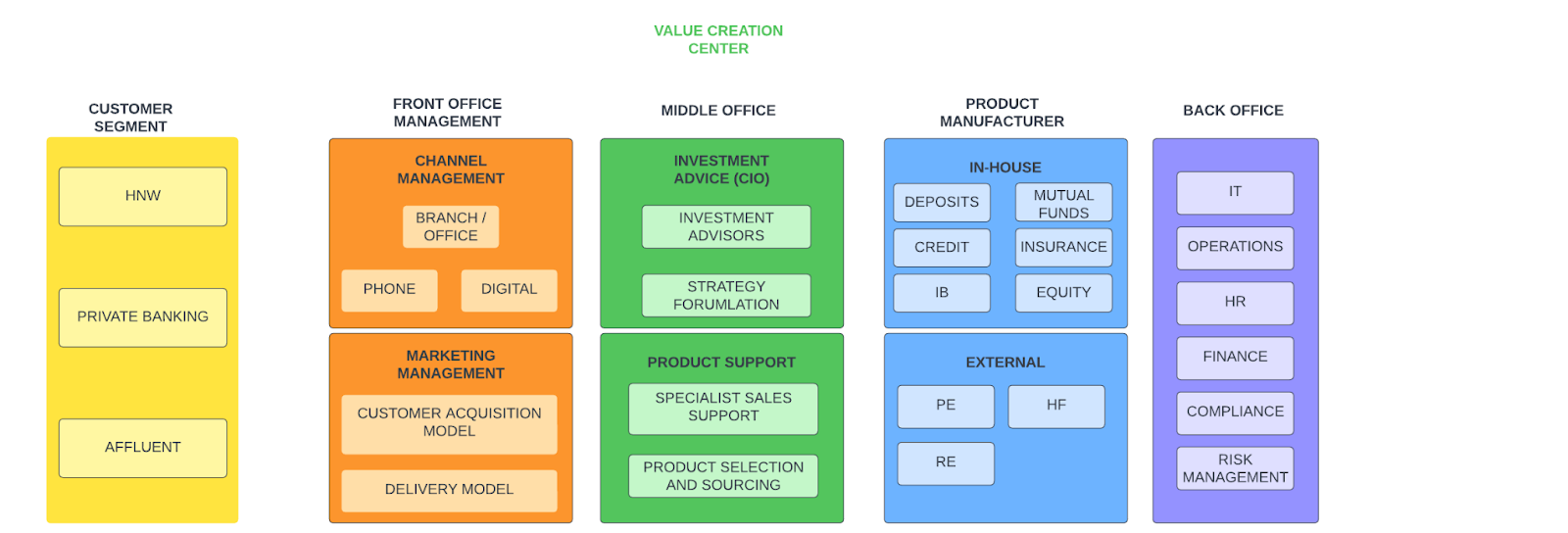

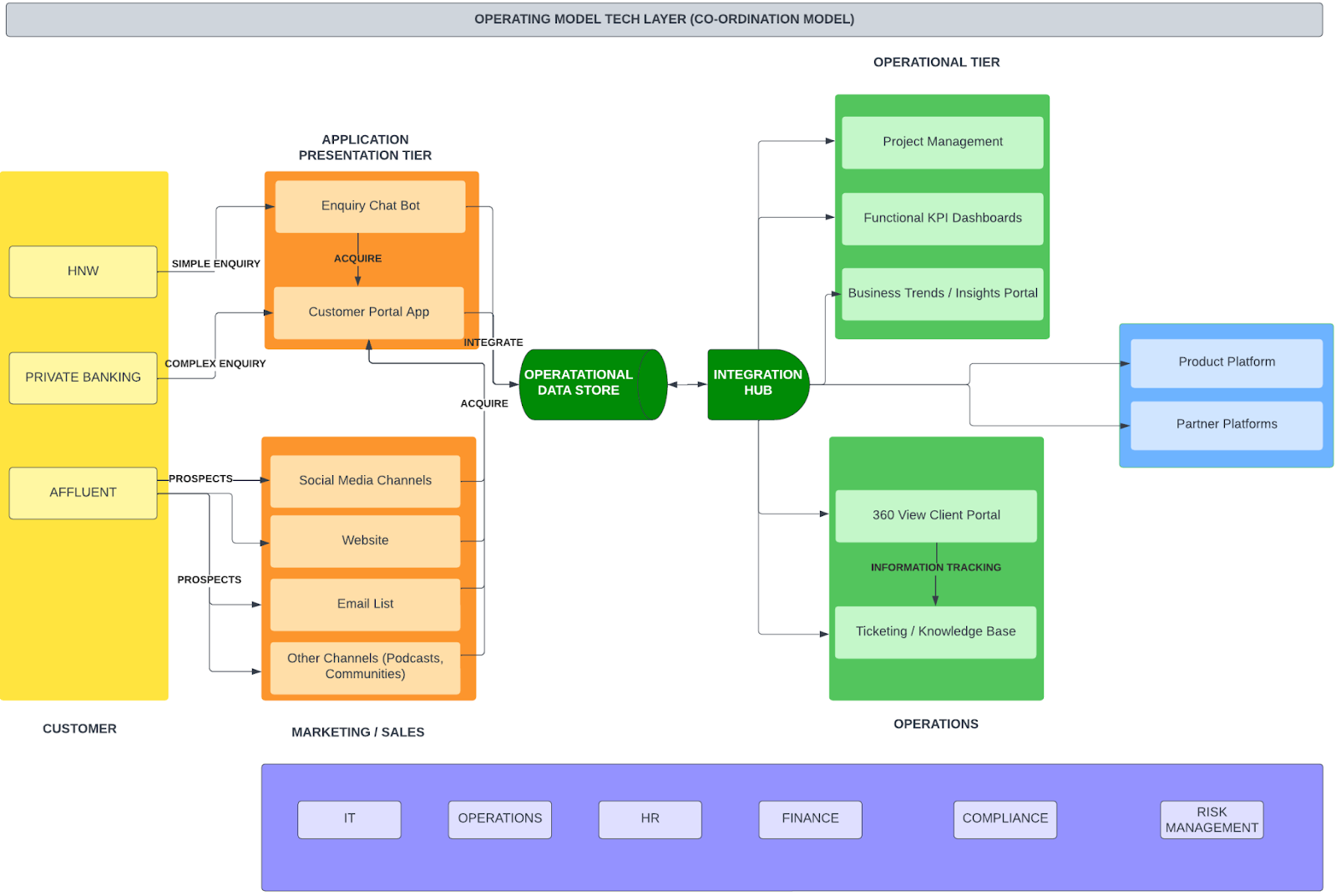

PROPOSED OPERATING MODEL – COORDINATION MODEL

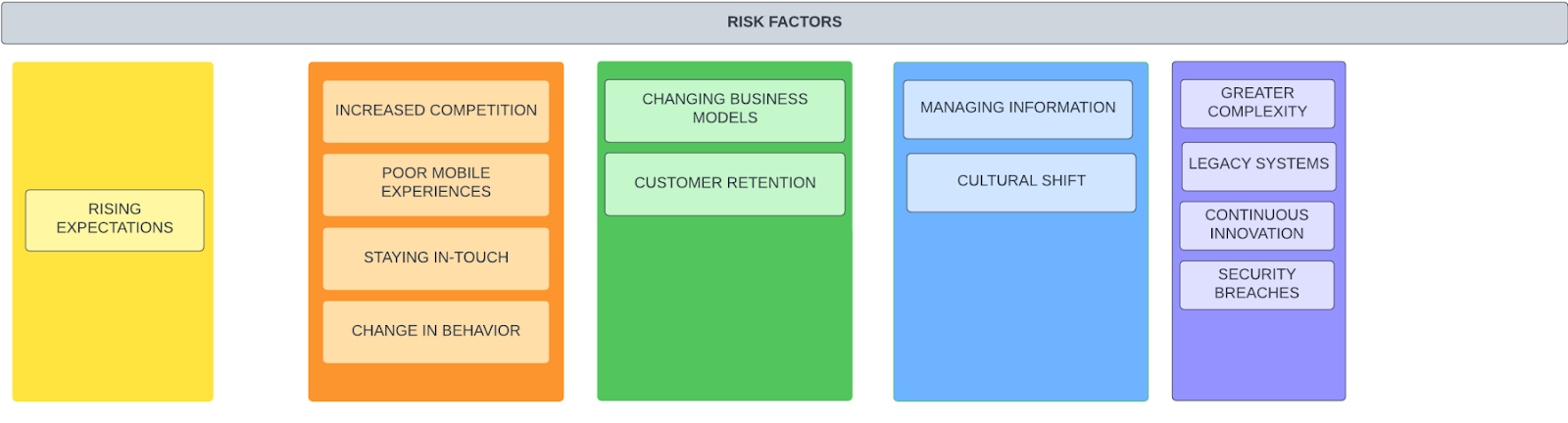

The diagram above is a representation of how a wealth management firm is able to structure itself for growth. Moving to a new operating model has challenges, as represented below, especially when trying to modernize towards a more technology-driven approach.

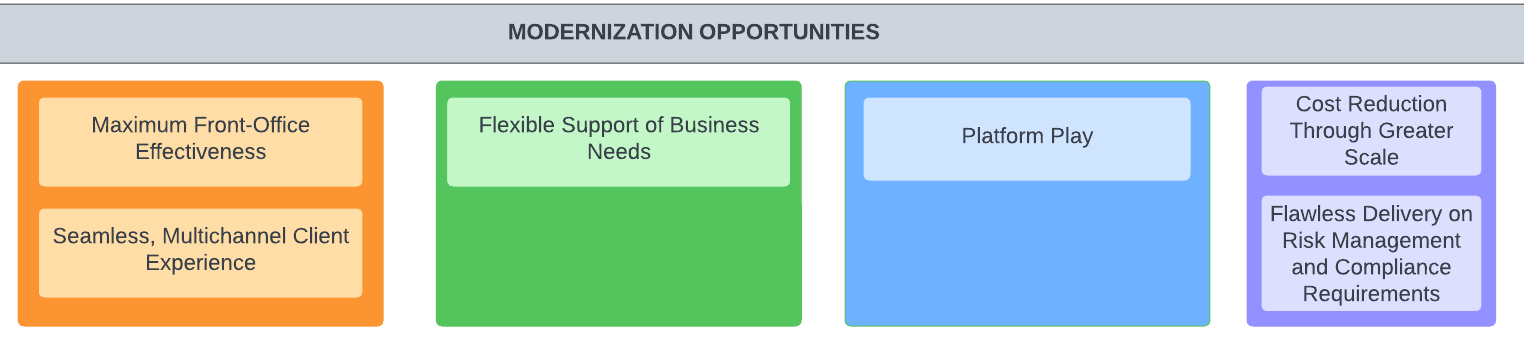

With challenges come opportunity, for Wealth Management firms moving towards a more modern approach provides many opportunities to capitalize on, as represented below.

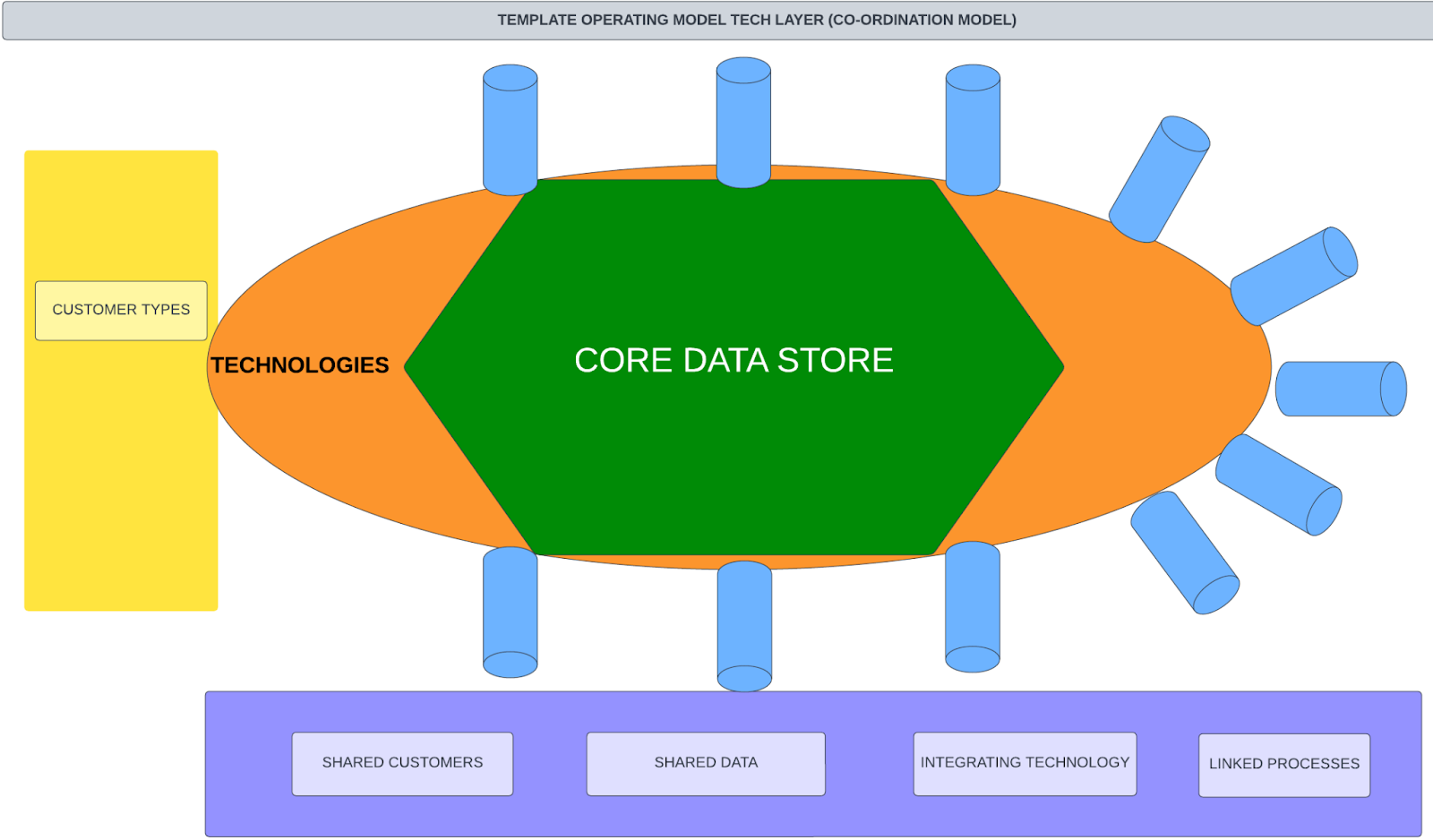

To capitalize on the opportunities above a coordination model would make sense to unlock to the growth potential of the organization. Below is a representation of the coordination model core diagram and what it could represent in a real-world Wealth Management Firm.

Download the Full Operating Model Here

Work with Skywalk Innovations

Would you like to learn more about how modernization would benefit your organization? Contact Skywalk to find out. Book a no-obligation information session with our team. Explore more ideas around technology and how it can grow your business.